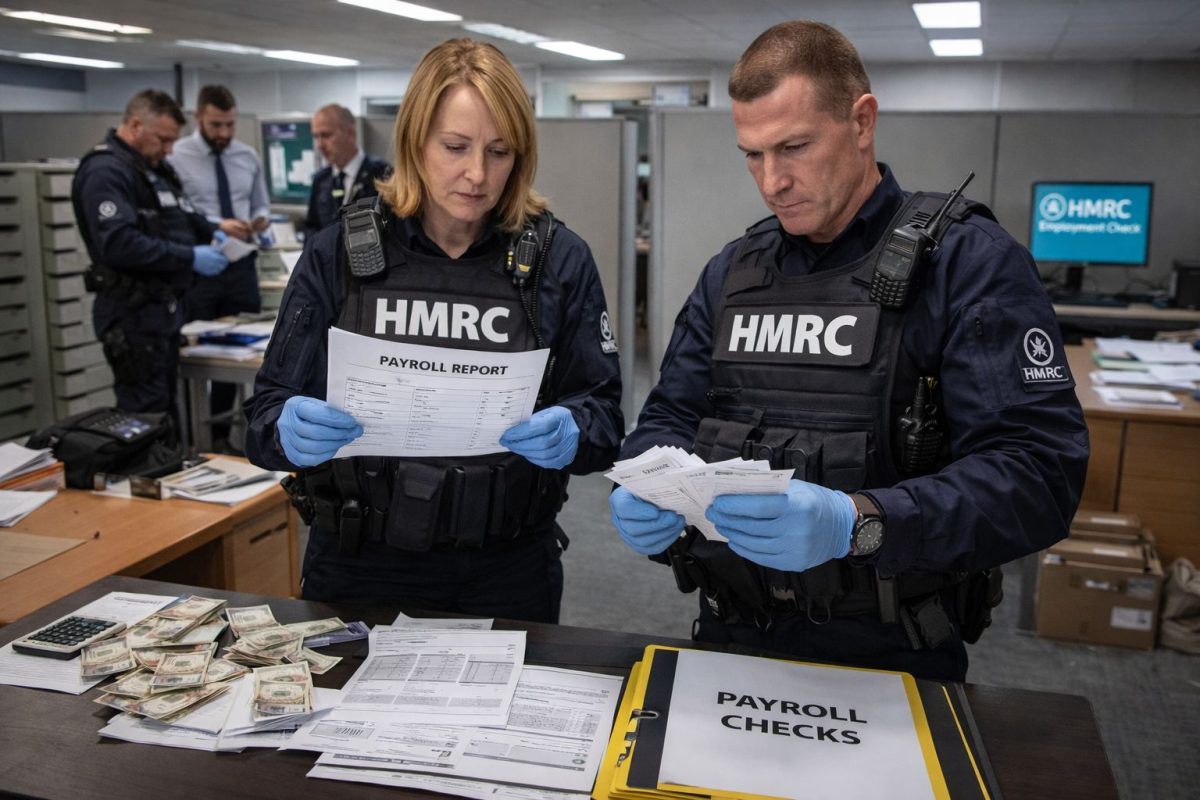

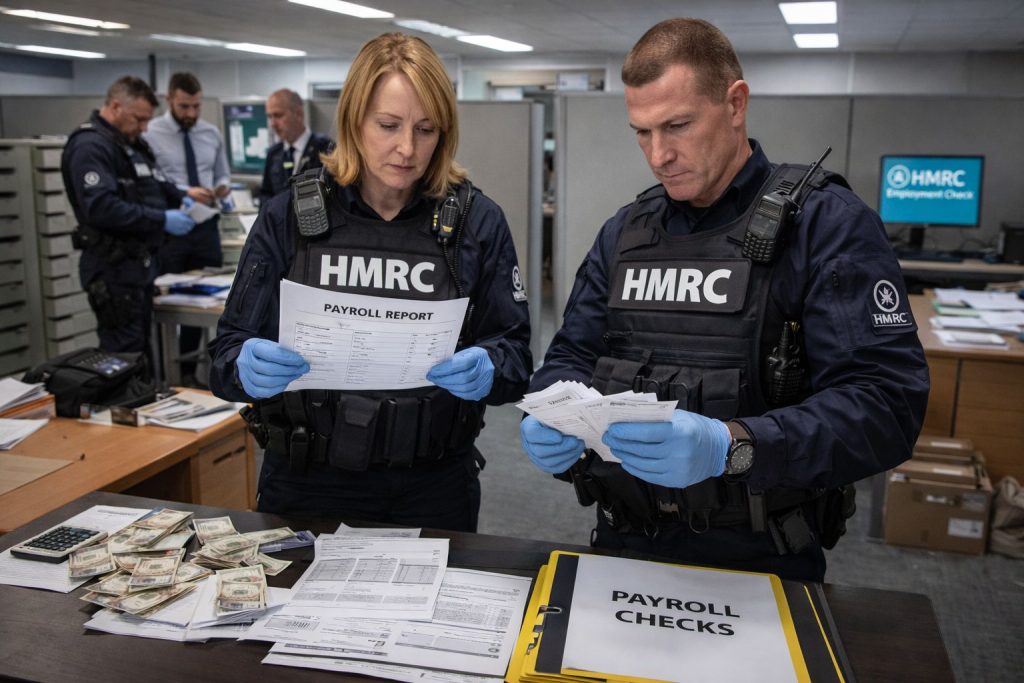

No employer expects an unannounced visit from HMRC. Yet across the United Kingdom, payroll compliance inspections are happening with greater frequency than at any previous point, and the consequences of being found unprepared have never been more serious. Whether you run a small business with a handful of employees or a larger operation with complex pay structures, the reality is the same: HMRC has both the authority and the appetite to look closely at how workers are being paid.

These inspections focus on one fundamental question: are the people working for your business receiving everything the law entitles them to? That means examining National Minimum Wage and National Living Wage compliance, Pay As You Earn records, National Insurance contributions, holiday pay accuracy, and every Real Time Information submission your payroll has made over a period that can stretch back years.

For any UK employer with payroll responsibilities, knowing how these checks work, what causes them, and what they measure is the first step toward keeping the business on the right side of an enforcement environment that is only going to intensify.

Table of Contents

ToggleWhat Happens During an HMRC Payroll Compliance Inspection

An HMRC payroll compliance inspection is not a paper exercise conducted by post. Officers can arrive at a business premises with very little notice, and in some cases, with none at all. On arrival, they introduce themselves, explain the purpose of the visit, and begin requesting records without delay. These typically include payslips, timesheets, employment contracts, PAYE returns, and documentation related to any deductions or benefits in kind currently in operation.

Staff may also be interviewed on-site to verify that what the records show reflects actual working arrangements. HMRC officers carry statutory powers to demand documentation, and any failure to cooperate can itself become a compliance concern on its own terms. Inspections can expand in scope as they progress, and findings can trigger retrospective reviews going back several years.

Not every payroll check begins with a physical visit. HMRC’s digital infrastructure generates automated flags based on discrepancies spotted in Real Time Information submissions, meaning many investigations begin with a formal letter rather than officers at the front desk. Either way, the process is official, documented, and capable of producing serious financial consequences when issues come to light.

Why HMRC Selects a Business for a Payroll Check

One of the most dangerous assumptions in UK employment compliance is that HMRC only targets businesses suspected of deliberate wrongdoing. In practice, inspections are triggered by a much wider range of factors, and many of them are entirely algorithmic.

HMRC’s systems continuously cross-reference declared pay levels and reported hours against sector wage benchmarks. Where a business consistently reports figures that fall outside what the system considers normal for its industry, an automated flag is generated without any human having made a judgment call. From that point forward, the business becomes a candidate for inspection.

Other common triggers include:

- Worker complaints submitted by current or former employees

- Gaps, inconsistencies, or anomalies in RTI submissions

- Reported pay levels that sit close to the National Minimum Wage threshold but include deductions or unpaid time that may push actual effective pay below the legal floor

- Operating in a sector with a historical pattern of non-compliance, including hospitality, retail, social care, cleaning, hairdressing, agriculture, and hand car washes

In a naming round published by HMRC in late 2025, 389 employers were found to have underpaid workers, resulting in £12.6 million in penalties recovered on top of repaid wages. In another round from October 2025, nearly 500 employers were identified for underpaying staff, with over £10.2 million in fines issued. These figures reflect how systematically enforcement has been scaled up. Being a law-abiding employer does not make a business immune from scrutiny if its payroll data looks irregular to HMRC’s monitoring systems.

The Most Common Payroll Compliance Failures

According to HMRC’s own reporting, the majority of wage underpayment cases do not arise from deliberate fraud. Most result from administrative mistakes, outdated processes, or a failure to keep pace with regulatory changes. The 2024 HMRC Annual Report found that 62% of wage underpayment cases were caused by errors in recording working hours rather than any intentional misconduct.

The most frequently identified compliance failures during inspections include:

- Failing to update pay rates when the National Living Wage or National Minimum Wage increases each April. The National Living Wage rose to £12.71 per hour from April 2026, and any payroll not updated from the date these rates came into effect is already in breach.

- Not paying workers for time spent travelling between client sites or completing mandatory pre-shift tasks.

- Deducting the cost of uniforms, meals, or equipment in a way that reduces a worker’s effective hourly rate below the legal minimum.

- Misclassifying workers as self-employed when the actual nature of the working arrangement makes them employees or workers under UK law.

- Failing to update rates when a worker turns 18 or 21 and becomes entitled to a higher wage tier.

- Using payroll software that has not been updated to reflect current statutory rates or that rounds pay figures incorrectly.

- Sleep-in shifts in social care where rest periods are treated as unpaid time, a recurring source of enforcement action across the sector.

As 5ive Magazine has noted in its coverage of UK employment trends, these patterns reflect a broader picture: compliance failures are often quiet and gradual, building over months or years inside organisations where no one has paused to audit the full picture of how payroll operates in practice.

Penalties, Public Naming, and the True Financial Exposure

When HMRC identifies underpayment, the financial exposure for the employer is significant. The business will be required to repay all outstanding wage arrears directly to affected workers and will face a penalty of up to 200% of the underpaid amount, capped at £20,000 per worker. Where arrears across the workforce exceed £500, the company can also be added to the government’s public naming list.

Public naming is not a minor administrative note. High-profile names on recent lists have included major care providers, national hospitality chains, and well-known retailers, sitting alongside hundreds of smaller businesses. The reputational consequences of appearing on that list frequently extend well beyond the financial penalty, affecting customer relationships, supplier confidence, and recruitment capacity in ways that can persist long after the fine has been paid.

In 2024 to 2025, HMRC opened 5,200 new cases and closed 4,800. Of those closed, around 1,200 resulted in workers receiving arrears, and approximately 750 penalties were issued, totalling £4.2 million. Where non-compliance is found to be deliberate or involves serious exploitation of workers, the consequences can include criminal prosecution and director disqualification.

The Fair Work Agency and a New Era of Employment Enforcement

One of the most significant changes to UK employment enforcement in recent years came into effect on 7 April 2026 with the launch of the Fair Work Agency. Created as an executive agency of the Department for Business and Trade under the Employment Rights Act 2025, the Fair Work Agency brings together several previously separate enforcement bodies under one unified structure.

The agency has absorbed the Employment Agency Standards Inspectorate, the Gangmasters and Labour Abuse Authority, and HMRC’s National Minimum Wage enforcement team. During the transitional year of 2026 to 2027, minimum wage enforcement will continue to be delivered by HMRC under a formal contracting arrangement with the Fair Work Agency. This means any enforcement correspondence carrying the HMRC logo during this period carries exactly the same legal weight as before.

The Fair Work Agency holds extensive powers: inspecting workplaces, demanding records, issuing Notices of Underpayment, pursuing civil proceedings, and even bringing tribunal claims on behalf of workers who choose not to pursue them independently. Holiday pay and Statutory Sick Pay have been designated as early enforcement priorities, making them as important to manage accurately as minimum wage compliance.

Holiday pay, in particular, has historically been one of the most error-prone areas of UK payroll. If overtime, commission, or irregular earnings are not factored into holiday pay calculations in line with current guidance, the issue can sit quietly in the background for months or years before anyone challenges it. The Fair Work Agency’s remit means that exposure across multiple pay areas can now be investigated within a single inspection visit rather than through separate processes.

For UK employers, this consolidation means enforcement is more joined-up, more proactive, and more visible than it has ever been.

Steps to Keep Your Business Payroll Compliant

Preparation for payroll compliance is not about bracing for an inspection and responding after the fact. It is about running payroll in a manner that would hold up to scrutiny on any given day, whether or not an inspection is expected.

Practical steps that give a business a sound foundation include:

- Auditing pay rates each January or February, well before the April increase takes effect, to identify workers whose pay will fall below the new National Living Wage or National Minimum Wage thresholds.

- Reviewing employment contracts to confirm that worker classification accurately reflects actual day-to-day working arrangements, with particular attention to variable-hours, zero-hours, and agency worker situations.

- Ensuring that all working time, including travel between assignments, mandatory training, and pre-shift preparation, is being recorded and paid at the correct rate.

- Checking that any deductions for uniforms, meals, accommodation, or other work-related costs do not reduce any worker’s effective hourly rate below the legal minimum.

- Retaining payslips, timesheets, and contracts for the full legal retention periods: three years for PAYE records and six years for National Minimum Wage documentation.

- Running internal compliance checks at regular intervals rather than waiting for a discrepancy to emerge externally.

Where a business identifies errors through its own internal audit, voluntary disclosure to HMRC is generally treated more favourably than non-compliance uncovered by officers during an inspection.

Why Payroll Accuracy Cannot Be Treated as a Once-a-Year Task

The environment in which HMRC wage raid payroll checks operate has changed fundamentally. Real Time Information requirements now mean that payroll data is submitted to HMRC every single time employees are paid, and the systems analysing that data are sophisticated enough to flag patterns that would have gone unnoticed a few years ago. Annual rate changes, evolving employment relationships, and the expanded reach of the Fair Work Agency all add to the compliance landscape that employers need to keep up with throughout the year.

Must Read : 5ivemagazine

The businesses that find themselves on enforcement lists are not predominantly rogue operators. They are, in the majority of cases, businesses where processes were not updated, where records were incomplete, or where no one stepped back to check that what was happening in practice matched what was being reported. That is a manageable risk, but only if payroll accuracy is treated as an ongoing operational priority rather than a task confined to April.